Categories

Buyers, SellersPublished May 1, 2025

Understanding Real Estate Closing Costs: What Every Buyer and Seller Should Know

Understanding Real Estate Closing Costs: What Every Buyer and Seller Should Know

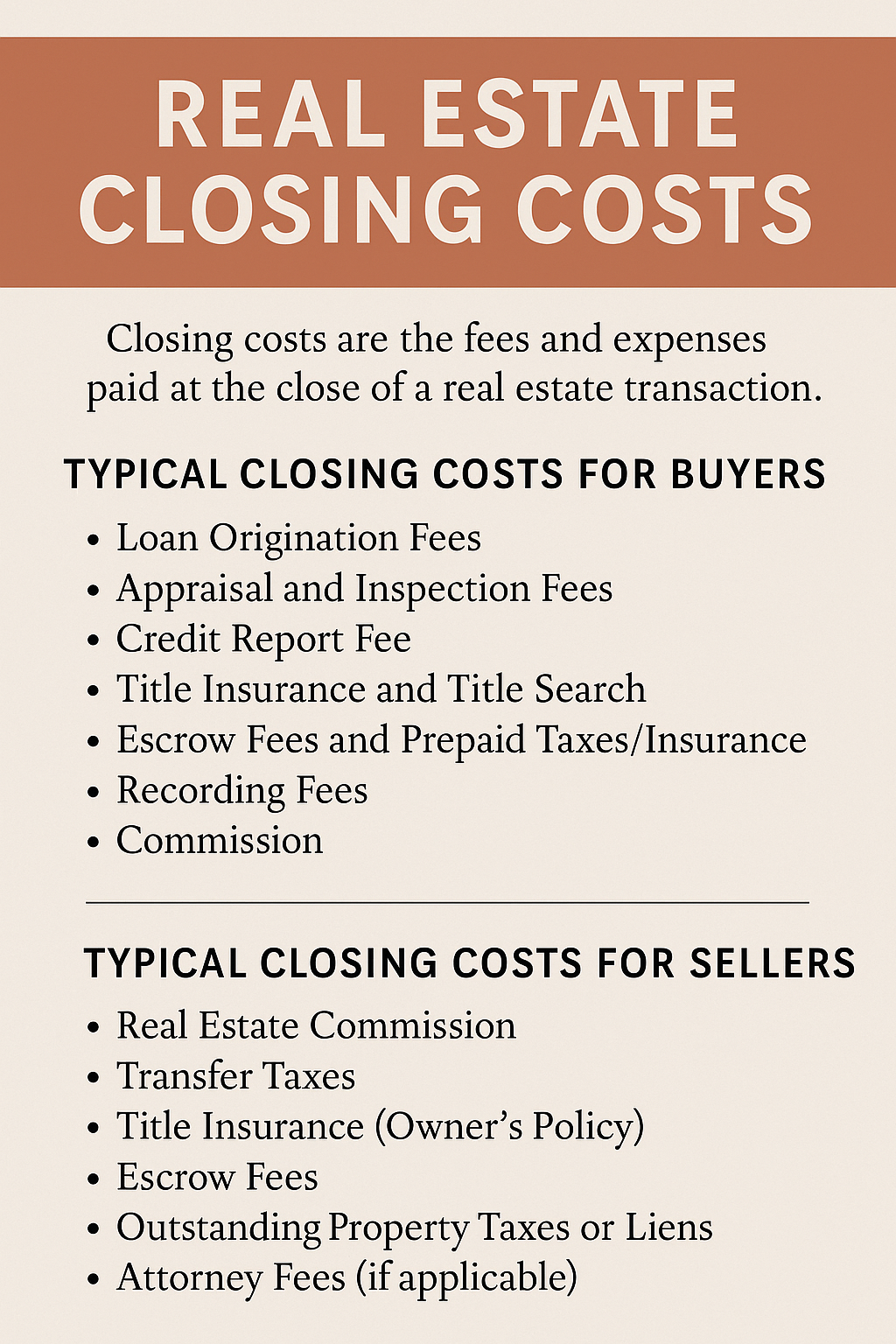

When buying or selling a home, the focus is often on the price of the property—but one of the biggest financial surprises can come at the very end: closing costs. These are the fees and charges paid to finalize a real estate transaction, and they can quickly add up.

One key piece of closing costs that’s getting more attention lately is the real estate commission—and who pays it. Traditionally, sellers have covered the entire commission for both their agent and the buyer’s agent. But that model is shifting, and in some transactions, both the buyer and seller may now contribute to commission costs.

Here’s what you need to know.

What Are Closing Costs?

Closing costs include all the administrative, legal, and financial fees that must be paid when a home sale is finalized. These typically range from 2% to 5% of the home’s sale price for buyers and can be even higher for sellers, depending on commissions and other obligations.

Typical Closing Costs for Buyers

-

Loan Origination Fees (charged by your lender)

-

Appraisal and Inspection Fees

-

Credit Report Fee

-

Title Insurance and Title Search

-

Escrow Fees and Prepaid Taxes/Insurance

-

Recording Fees

New Trend: Buyer's Agent Commission

In some cases, especially in today’s evolving real estate market, buyers may be asked or required to pay their agent’s commission directly—rather than having it paid by the seller. This means buyers need to factor in agent fees as part of their closing costs or overall home-buying budget.

Typical Closing Costs for Sellers

-

Real Estate Commission (Seller’s Agent and possibly Buyer’s Agent)

-

Transfer Taxes

-

Title Insurance (Owner’s Policy)

-

Escrow Fees

-

Outstanding Property Taxes or Liens

-

Attorney Fees (if applicable)

Traditionally, the seller pays a real estate commission, which is split between their agent and the buyer’s agent. However, that’s not always the case anymore.

Changing Commission Models: Shared or Buyer-Paid Fees

Real estate commission practices are evolving, particularly in light of recent lawsuits and growing demand for transparency. It’s now more common for:

-

Buyers to negotiate directly with their agents regarding compensation.

-

Sellers to offer reduced or no commission for the buyer’s agent in the listing.

-

Buyers and sellers to share commission costs, as part of the overall negotiation.

This change means:

-

Buyers need to budget for their agent’s fee, especially if it's not covered by the seller.

-

Sellers might have lower total closing costs, but could make their property less attractive if they don’t offer a commission incentive to buyer agents.

Who Pays What? It Depends

In any real estate transaction, everything is negotiable—including who pays the commission and closing costs. It all comes down to the contract and local norms. In hot markets, buyers may offer to cover more costs (including agent commission) to make their offer more competitive. In slower markets, sellers may be more willing to sweeten the deal.

How to Prepare

Whether you're buying or selling, here's how to prepare for closing costs in today's market:

-

Ask your agent for a closing cost estimate early in the process.

-

Understand how your agent is being paid, and who is responsible.

-

Shop around for lenders, title companies, and other services to potentially save.

-

Negotiate closing cost responsibilities in your offer or contract.

-

Be ready for flexibility—commission practices are changing, and each deal is unique.

Final Thoughts

Closing costs are a critical part of real estate transactions, and commission structures are no longer one-size-fits-all. Buyers and sellers should understand not just what the costs are—but who’s expected to pay them. Talk openly with your agent about commissions, ask the right questions, and factor these expenses into your overall budget.

The more you know going in, the smoother your closing will be.

Andrew Bartlett

Team Leader | Owner | Realtor | Bartlett & Associates | Keller Williams Elite | PLACE

or another way